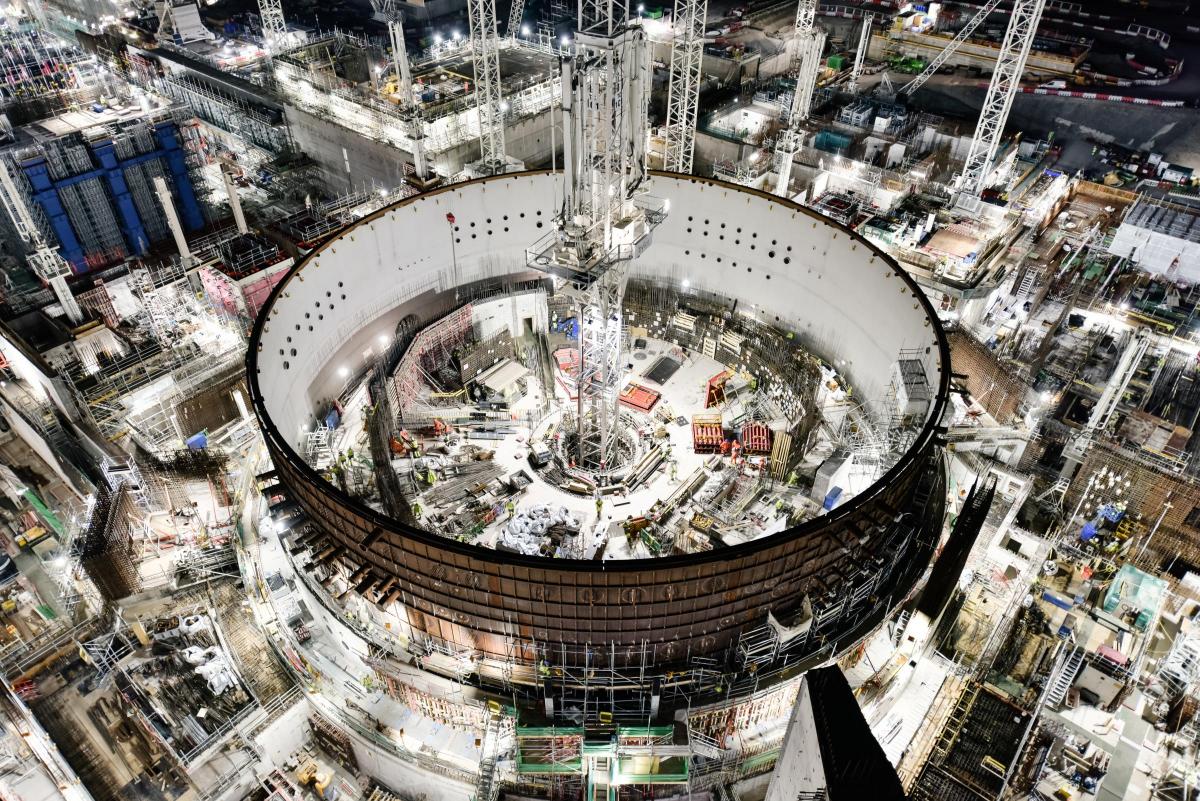

The Brexit British Energy Security Strategy is launched today, and it puts new nuclear power front and centre. 24GW of new nuclear by 2050, substantial new funding (despite none being available for energy efficiency) and an ambition to build one reactor a year instead of one a decade.

There are huge feasibility issues here – nuclear power stations suck in huge numbers of numbers of construction workers amidst an ‘ever growing skills gap’ in the industry. Small modular reactors (SMRs) are to form a ‘key part’ of the pipeline. But up until late last year there was no legal definition of an SMR and the UK regulatory approach had not even been decided. In November, Rolls Royce submitted an SMR for assessment but the process takes around four years.

But setting these and other issues (like the fact that nuclear power stations are potentially disastrous in conflicts as the invasion of Ukraine is showing) aside, what about the cost of new nuclear?

The contract for difference deal for Hinkley Point C sets a price of £89.50/MWh, roughly double the government’s own estimates of the generation costs of onshore wind and large scale solar PV, and well above that of offshore wind. Both government and industry argue that this is a ‘first-of-a-kind’ cost and that with a larger fleet using an established design, costs will come down to become competitive.

However, a more important development on costs is the government’s move to fund new nuclear using a regulated asset base (RAB) approach. The RAB approach has long been used to fund electricity and gas networks – companies borrow to build infrastructure and consumers have to pay a certain amount every year to cover these capital costs, with the amount they pay being regulated by Ofgem.

The big idea with the RAB approach is that it reduces risks for companies by sharing these with consumers. This includes construction risks, and this matters as there have been big construction cost overruns on recent European nuclear projects. In theory the RAB approach should reduce how much companies pay to borrow – the ‘cost of capital’. Since nuclear is very, very capital intensive with relatively small running costs, the cost of electricity from nuclear is highly sensitive to the cost of capital.

There are questions about why a RAB approach should be taken with one kind of generation while not with others; as a 2019 National Infrastructure Commission report pointed out, this is an implicit subsidy for nuclear compared with other technologies, above and beyond any CfD FiT.

There are also dangers that consumers start paying upfront for the construction of planned plants that in the end are never built because demand is lower than expected or because other kinds of capacity grow more than expected. This has been the US experience where a RAB approach for nuclear has led to consumers paying billions of dollars for plants that were never completed.

Beyond this, there is a risk that institutional investors, to whom developers will turn for financing new nuclear plants, will not want to get involved. Institutional investors are under increasing pressure on environmental and social governance (ESG) and some are not convinced that nuclear makes the cut.

But there are also questions of how far a RAB approach will actually reduce costs. The government expects that compared with the CfD FiT approach for Hinkley C the RAB approach will reduce costs by £10/MWh. The best guide to this is how this approach has worked in the area where it has already been applied for years – i.e. energy networks. The short answer is that regulators have struggled to get value for money because of ‘asymmetric information’ – i.e. companies know more about real costs, including the costs of capital, than regulators do, and despite lots of efforts to stop them, often game the system to earn higher profits than they should. Networks are a low risk business, and companies in the industry should be earning relatively low, single-figure returns on equity. But the experience of the 2010s was that network companies were earning up to 12%, and an average 19% profit margin.

So even a RAB approach may not offer real value for money on nuclear. Ultimately, the big, rapid falls in the costs of renewables have come about because of competition. Nuclear power plants are too big and risky (even ‘small’ modular reactors are actually pretty big) to be built in any other way than through a negotiated process between states and a very limited number of large companies. By giving nuclear such a central role, the BESS may provide a long-term vision to help get off gas in electricity generation, but it is a risky and potentially costly one.